Trading Articles

Downside Protection With Double-Digit Returns By John Manley

This strategy has potential for double-digit returns with a large built-in hedge. Current market conditions have set up a unique opportunity to build a conservative portfolio that will profit even if the market falls by a certain percent, stays flat, or eventually rises over the remainder of the year. It goes without saying we have witnessed the most violent and dramatic market moves of the last 75 years of late. After falling a whopping 38.5% in 2008, the Standard & Poor’s 500 is already down another 21% in the first eight weeks of 2009. How does a traditional investor defend himself against this kind of market volatility and still have a chance of making money?

THE PREMISE

What if you could build a diversified portfolio of quality stocks or exchange traded funds (ETFs) with a large built-in hedge of anywhere from 20% to 40%below entry prices and still pull off double-digit gains at the end of the year, even if the markets go nowhere? You can. Welcome to the in-the-money covered-call portfolio! What makes this strategy particularly attractive right now is that we have two favorable conditions present — depressed stock prices (subjectively, prices could fall further, but I am about to show you that’s okay) and high premiums for options (elevated implied volatility priced into options). One of the other desirable attributes of this strategy is that it is relatively low maintenance. It is perfect for the busy trader or investor who doesn’t have time to check the markets all the time — and it keeps transaction costs down.

THE MECHANICS

An in-the-money covered call is a simple two-part strategy. Part 1 is the purchase of your chosen under-lying instrument (stock or ETF). I will address the criteria for selection later. Part 2 involves selling a long dated call option below the purchase price of the stock/ETF. How far below you sell a call is subject to your analysis and desired return. The further below your stock purchase price, the greater the hedge (protection) but lower the overall return. The risk/reward tradeoff is at play here.

But why would an investor commit himself to sell a stock below his purchase price? The answer is quite simple: premium collected. When we sell an in-the-money call option, there are two components of the total premium collected: intrinsic value (the difference between the strike price of the call you sell and the current stock price) and extrinsic value (the time value factored into the option premium). If the stock begins to fall toward the sold call’s strike price the stock will lose money, but the option intrinsic value will accumulate profits because we are short the option. Because of the canceling effect between the stock price and the intrinsic value of the option premium, your profit will come from the extrinsic (or time value of the option), which will erode as time moves forward. We are acting very much like an insurance company that has sold a policy.

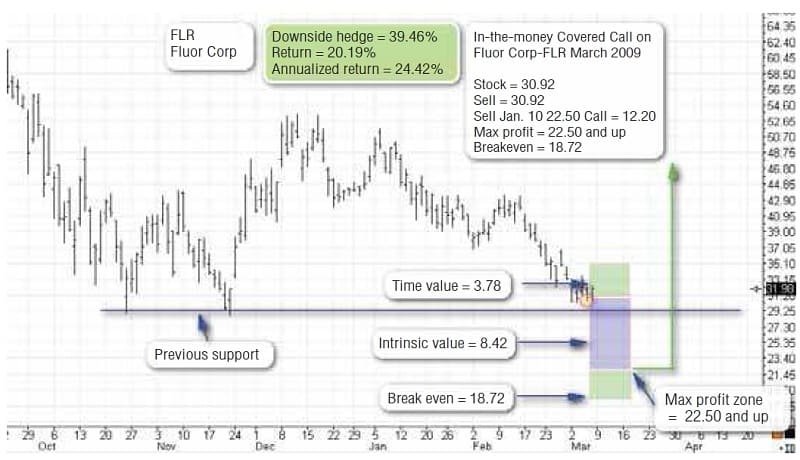

Let’s look at a current example. On March 4, Fluor Corp. (FLR) closed at $30.92, very close to its 52-week lows of $28.60. Let’s say you like the long-term prospects of this company, but have near-term and intermediate concerns about the stock’s ability to sustain a rally because of current market conditions. FLR also pays a$0.125 quarterly dividend. Armed with your research, you would buy FLR at $30.92. You plan to hold the stock until the end of 2009 at the earliest, as this is an investment, rather than a short-term trade. Now, with the stock at $30.92, which call option do you sell against it?

Because you want to hold until the end of the year, you are going to target the January 2010 options and look at the $25,$22.50, and $20 strike prices (Figure 1). As you can see from the table, if you sell the $25 strike against the stock, it will give you the greatest return but less downside protection. The $20 strike price will give you the greatest hedge, but also a lower return. For the sake of this example, you are going to sell the $22.50 strike against the stock. You now go into the market and collect $12.20 in premium for the January 2010, $22.50 call option.

Figure 2 breaks down the play. Remember, you collected$12.20 in total premium. Of that premium, $8.42 is intrinsic value (blue bar). The $8.42 is the difference between $22.50 (the strike price) and the current stock price, $30.92. The remaining premium collected is $3.78 (the green bar), which represents the time premium and the maximum profit on the play.

Let’s break it down a little more. We bought the stock at$30.92 and collected $12.20 in premium; the cost base (breakeven) on the play is $18.72, a full 39.46% below the current price. You have a built-in hedge of almost 40% when the play begins. That may help you sleep a little better as the market gyrates back and forth. Your maximum profit will be maintained as long as the stock is above $22.50 at expiry. The stock can fall another 27.23% and you will still have maximum profit. On an unleveraged basis (without margin), your return on the play is 20.19%, or 24.42% annualized. In a margin account, your return would be double at 40.38% (less interest costs).

Let’s recap:

- Bought stock at $30.92.

- Sold January 2010, $22.50 call option and collected 12.20 in premium.

- Maximum profit is $3.78 per share or 20.19% (24.42% annualized).

- Built-in hedge (breakeven) is 39.46% below purchase price.

- Maximum profit hedge = 27.23%. Stock can fall by this amount and you will still receive maximum profit.

As a side note, you can theoretically sell options against the stock with closer months (say April, June, July, and so forth) and collect more premium throughout the year, but that changes the premise of this strategy. It changes how much downside protection you are able to get and how much premium you can keep. You also become more of an active trader, and as market conditions change, there may be times throughout the year when it may not be appropriate to sell in-the-money calls against the stock. For simplicity’s sake, we are going to look at this as an investor’s portfolio.

Suggested Books and Courses About Hedge and ETF Funds

Experienced option traders will recognize that an in-the-money covered call (or any covered call, for that matter) is also a synthetic short put (selling a put to open a new trade). Why bother buying the stock and selling a call, when you can sell a put instead and have just one transaction? You can, but with the scenario we are presenting, we are going to assume the stock may also pay a dividend, and for some registered accounts such as Individual Retirement Accounts (IRAs) (in the US) and Registered Retirement Savings Plan (RRSPs) (in Canada), selling puts may not be allowed, or the investor may not have permission to sell puts or calls uncovered in their accounts. This is a way around it.

RISKS AND OPPORTUNITY COST

As we stated, the premise of the in-the-money call portfolio is to build a conservative, defensive portfolio that can withstand volatility, let you sleep at night, and still deliver healthy double-digit returns even if the markets go nowhere. It is a great strategy for the current market environment. The greatest risk of the strategy is the fundamentals if one of your positions dramatically changes for the worse. If that is the case, the position should be reassessed and possibly removed from the portfolio. Remember, your position has a large built-in hedge. If such a fundamental downturn happened to the example I presented earlier (FLR), it could fall another 40% and you could still get out at breakeven by expiry.

What are the opportunity costs involved with the in-the-money covered-call strategy? There is always the possibility that the markets could take off to the upside, and because this strategy has a defined profit, any movement above that fixed-profit point will be an opportunity cost. With respect to the FLR example, it would mean any gain above 20.19% by expiry in January 2010. On the bright side, if the stock does shoot up, you may be able to shut the trade down right away for 90% to 95%of its maximum profit potential, rather than wait months for expiry. This would give you banked profits and fresh capital to deploy elsewhere.

Once again, the premise of the portfolio is not to be an active speculator, but to pump out healthy, hedged returns. In the current market environment, I can’t think of any investor who would not be happy with returns of 20% or more by the end of the year without developing an ulcer in the process.

CANDIDATE SELECTION

The next question to ask in our analysis is what kind of candidates are best suited for this strategy. Since this is a neutral to bullish strategy with downside protection built in, you will want candidates that should rise in price over time, although that is not necessary. When doing your homework, make sure the fundamentals of the underlying instrument you select are sound and prospects are good. When I apply this strategy, I will start the selection of a candidate, then apply my technical analysis system to look for an entry on a swing low. As of this writing, pretty much everything is hovering around all-time lows, with the reality that they can go lower. If I can put on positions around here with another 20% to 40% downside protection, I can breathe a little easier with the portfolio.

Criteria recap:

- Stocks and ETFs with solid fundamentals and prospects

- Dividend paying for added return

- A liquid and deep options market attached to the underlying tradable

- Elevated option premiums (due to selloff and market volatility)

- Underlying priced from $25 to $60 (subjective on the top end)

What you are looking to do is build a diversified portfolio of stocks (ETFs and indexes can be included). The ultimate selection and number of candidates would be based on your own research. The in-the-money covered-call portfolio can represent a portion of your overall portfolio or your complete portfolio. It is a personal decision.

HERE’S ANOTHER EXAMPLE

I have built a random portfolio of stocks and ETFs as of March 9, 2009. The purpose of this portfolio is to illustrate the downside protection and potential returns of a group of stocks/ETFs. It should not be interpreted as a recommendation or advice to buy any of the securities in the portfolio.

Example 1

This portfolio features seven positions in total. It is an unweighted example in which we went into the market and simply bought 500 shares of each issue. As you can see from Figure 3, the portfolio has the potential to throw off an 18.47%(unleveraged) return by January expiry with an average 34.03%downside protection overall. The average downside protection percentage is for illustration purposes only, as each issue will have its own unique protection. The return of 18.47% does not take into account potential dividend payouts, which would boost the overall return.

In a margin account, the return would be approximately double (36.94%) less interest costs. Commissions and slippage have not been taken into account. The MaxPP column tells you how far the stock can fall in percentage terms and still give you maximum profits. The risk column is the total cost of the stock less the premium collected with the sale of the call option. It also represents the breakeven (cost base) of the play.

Example 2

This example (Figure 4) is the same portfolio, except I have attempted to weight each component equally with respect to dollars at risk. With rounding calculations, the return is just slightly less at 18.44% unleveraged.

OPTIONS EXPIRY

When option expiry rolls around in January 2010, you will have a few alternatives available to you. If stock prices are:

- Above the strike price you sold, you can simply let the stock be called away, and you will be finished with the play at maximum profit.

- Above the strike price you sold and you want to retain the stock, you can buy the short call back. It may cost you $0.10 to $0.15 in extrinsic (time value) to close the play. Your return will be very close to maximum profit. Now you are free to own the stock unhedged, or begin selling calls against the stock again.

- Below the original call strike price, the option will expire worthless. You can reevaluate the stock at that time and see if the fundamentals still measure up, as the stock is showing weakness. If you decide to keep the stock you can hold it unhedged, or sell calls once again to lower the cost base even more.

SIMPLE HEDGED PORTFOLIO

As of this writing, the talking heads, advisors, and financial media are scrambling to make sense of the current market environment and are generally at a loss as what to tell investors to do. Many investors are fleeing the market after the indexes have fallen 54% off their highs and vowing never to return. Personally, I think this is a big mistake. With a little knowledge, risk management, and common sense, simple hedged portfolios can be built for every investor. These portfolios come with large downside protection, the ability to collect dividends, and still garner double-digit returns, even if the markets go nowhere.

Now is the time for investors to shift their thinking in how they approach the markets. Traditional investment methods may be ineffective going forward and take a great amount of time and your life, just to get you back to the starting gate. Technology and knowledge have opened a whole new dimension for investors to explore for risk-managed returns. The in-the-money covered call portfolio is a great example. If you are interested in a free copy of the in-the-money covered-call return calculation spreadsheet, please email me.

John Manley is a professional derivatives trader. He manages a private option-based hedge fund for a group of high net worth individuals. Manley also engages in advisory and educational services for individuals and institutions on the proper use of exchange traded options for superior portfolio returns and risk management. He holds the Derivatives Market Specialist designation from the Canadian Securities Institute.