Trading Articles

Profits Can Be Painful: Trading Psychology and Exit Discipline

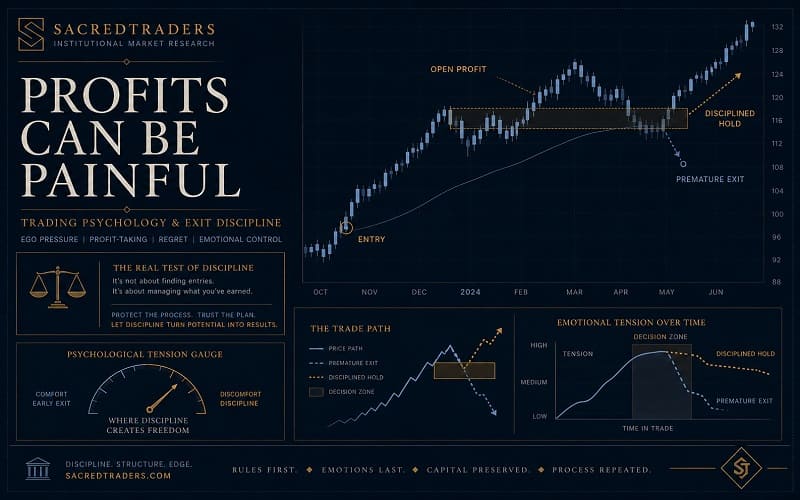

Profitable situations can provide us with as much pain and anguish as the unprofitable if we work it right. If they are tied to our self-esteem—if we are trading ourselves instead of wheat or GM—a paper profit presents us with a real problem: to take it, book it, feel good, and perhaps see it soar to extremes, leaving us kicking ourselves for exiting too early, or perhaps to see the profit erode away and not be takeable at all. Ego involvement and a lack of a mature methodology can only result in pain and regret for the unequipped and uneducated trader. One thing is certain: If perfection is your standard or goal, art (or machine tools or theoretical mathematics) is the field for you. Not Wall Street.

We have seen how utter ruin can come about when a man perceives any need to alter his opinion as an attack on his ego. He can also be hurt when he is on the profit side, and for much the same reasons. Let us say that Ed Smith buys a contract of soy beans at around $2.90 a bushel. He has put up a deposit of $1,000 against his contract of 5,000 bushels. Each cent that soy beans advance will therefore mean a gain of$50 or 5 percent.

Let us suppose that soy beans do advance (as they did at this particular time). What is Ed to do when beans are selling at $3.00 only a few weeks later? Obviously, bidders have perceived the possibility of a shorter supply of soy beans or (you could put it) a greater demand. If Ed sells out now, he will have a good profit; in fact, he will have made 50 percent on his capital of $1,000.

It is hard to lose money. But it may well be that the sufferings of the trader who has a big profit are more intense than those of a loser. What to do? To sell the beans means securing the immediate profit. But if one sells them now, what is to prevent them from going higher? Then one would be left standing on the dock, with a strong feeling of having missed the boat. Then again, if they were not sold, suppose they were to react and end up again at $2.90—or $2.80.

This is a problem in commodity trading and in money. But it is also, and most importantly, a problem concerning the self. Unless one can muster some defenses, it’s going to hurt too much to see beans go up after they have been sold, and it will also hurt too much to see them go down if one decides to hold.

There are some possible defenses. They will cost more money, perhaps, but they may save the ego. One can always argue that the commodity markets are manipulated. Or that the information underpinning the decision to sell (or not to sell) was inaccurately or dishonestly reported. These defenses make it clear that whatever happens, it’s “not me” that was at fault. It’s somebody else’s fault.

We do this very often in other life situations. We can keep looking pretty good to ourselves if we can externalize the blame. We lost the job because the boss was looking for a place for his nephew. We lost the girl because her mother influenced her against us. We failed in the examination because the professor asked some very unfair questions. In any case, it was “not me.”

Advanced Books and Courses on Trading Psychology

It appears that some sort of sleight of hand on the part of professional market riggers was to blame. This is not the way to correct past errors or improve one’s trading methods. Let us go back to soy beans. Beans, having advanced from $2.90 to $3.00, now run up to $3.15, giving Ed Smith a profit of 125 percent. If the tension was extreme before, think what it must be now. Consider the ups and downs of the emotional barometer as beans react to $3.05, advance to $3.30, decline to $3.20, etc. The fact is that on this move soy beans eventually advanced a good deal more than $1.00, a gain of over 100 percent, in only a few months.

What a wonderful opportunity to take a big profit! Yes, but how many men would have the stamina and assurance to see it through? How many would be able to face the possibility of losing part of the gains? There are, I believe, many market traders who would find it easier, all things considered, to sell out the soy beans when they first reached $3.00 than to let soy beans go to $3.50 and then sell out at $3.20. In this second case, one would make a good deal more money, but it is much easier to sell on the way up than to sell after the price has gone against you for 30 points. In the first case you can always say, “Well, I got my profit; let the other fellow have his,” which leaves the self-esteem looking pretty sharp. In the second case one is forced to face the fact that one did not call the turn at the top. And you must realize by now that the difference of a few hundred dollars is as nothing compared with the pain of a hurt to the ego.

It all depends on how you measure your values. If you insist on using a fantasy of perfection for a mirror, you are bound to be threatened by the danger that the reality will intrude itself on the pleasant image. There is no reason you need to regard selling out at something less than the top as a defeat. And if you let yourself be worried into premature selling every time you have a small profit, you will find your equity shrinking as the commissions and inevitable losses mount in your trading account.

- Part of Book: Winning the Mental Game on Wall Street By John Magee