Trading Articles

Forex Arbitrage Strategies: An Analytical Review of Joseph James Gelet’s Guide

What should traders understand about arbitrage as it pertains to the forex market? Foreign exchange arbitrage is a hotly debated topic in the forex community with many unknowns, as successful arbitrageurs may not have the incentives to disclose their methodology until after it is no longer effective. Since the concept of arbitrage is so intriguing, traders are attracted to it but do not have resources to find quality unbiased information on the subject. We will discuss some of the most important aspects that traders should understand about arbitrage as it pertains to the FX market.

FX VERSUS OTHER MARKETS

Forex markets are not traded on an exchange; forex is an over-the-counter (OTC) spot market where participants exchange one currency for another. Since there is no exchange, the price that one bank may quote for an FX rate may be different from that of another bank. However, with technological developments such as the increase of Internet speeds, computing power, and pricing algorithms, FX prices can be obtained from multiple sources. Further, since banks also trade with multiple counterparties, a close to market price can be created. This means the difference in price between different FX liquidity pools could be minimal. Price discrepancies may only exist for a minuscule length of time (in fact, measured in milliseconds), and it is questionable whether these discrepancies provide ample opportunity for profit.

BANKS AND ARBITRAGE

If there were a way to profit in the FX markets with little risk, why wouldn’t the banks be taking advantage of it? The answer is more complex than it seems, because banks create the FX price and the algorithms involved in the price creation take numerous variables into consideration. In addition, banks typically attempt to make markets and do not normally engage in proprietary FX trading on behalf of the bank. So their role is usually that of finding the best price for their clients and profiting by either charging a commission or a spread markup.

Banks have many ways to profit from FX without needing to utilize arbitrage. For example, retail exchange rates offered to smaller clients may have a spread of up to 1% of the total transaction or more, which is pure profit for the bank. Generally, customers such as travelers exchanging small amounts of money don’t mind paying such costs (but then, they don’t have much choice!). Banks don’t profit a lot on each deal, but due to the large amount of volume of small transactions, this can add up to a good profit.

Since they have a near monopoly on this activity, they may not see a need for investment in highly sophisticated arbitrage trading that has its own unique set of risks. These transactions are one way that banks profit in the FX market, but it provides a good example why banks are not anxious to develop proprietary arbitrage trading models. Another factor to be considered is volume, which is typically opaque to the average customer. If a bank has an order to sell 100 million EUR/USD or more, it may not be available at the current price. They may have to sell EUR/USD to multiple counterparties, each at a different price, providing their client with an average fill price.

By obtaining the best possible price for their client, they can charge a commission or possibly mark up the price by one pip while still providing an excellent price to the client on a large order. If in this “price discovery,” a bank found an off-market price that would be considered arbitrage, they may take it but pass it to their client mixed with the other trades included in the average fill price. (We’ll discuss price discovery in a few paragraphs.)

This would be considered a wholesale price in other industries; companies may purchase products from manufacturers and mark up the price for a small profit. It isn’t much different here, except it is done in real-time and calculated by use of pricing algorithms. So while banks do not necessarily engage in proprietary arbitrage, they have an incentive to constantly find the best forex price for their clients.

HOW A FOREX PRICE IS CREATED

Banks have millions of clients who want to exchange currencies, known as “deliverables” (for example, you want to send funds from Europe to the US, whereby Deutsche Bank may exchange your euros for US dollars at JP Morgan). Since banks have such a large demand for FX known as “real money flows,” they need to actively trade forex in order to exchange these funds on behalf of their customers.

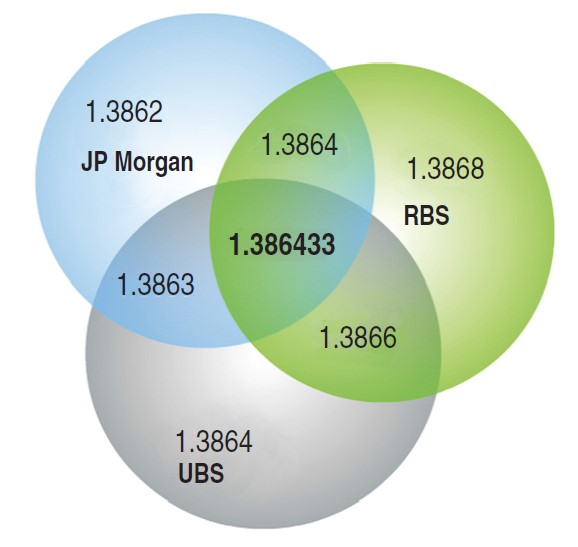

Figure 1 shows how a forex price is created. Banks have customers who want to trade their euros for dollars and vice versa (EUR/USD is used in this example). Each bank then sends quotes to other banks, a process known as “price discovery,” which can happen in seconds. Previously, this may have involved a bank trader calling several banks to get information about the offered or bid rate. Price discovery is usually done by sending bids and offers at different price levels to see if there are any takers. If there are none, the bank may have to buy at market rates already bid and offered.

In this example you can see the price between two individual banks, Royal Bank of Scotland (RBS) and Union Bank of Switzerland (UBS), is 1.3866. This differs from the price between UBS and JP Morgan, which is 1.3863. It is also different from the price between JP Morgan and RBS, which is 1.3864. The number in the middle of the Venn diagram where all three circles intersect would be the market price. As you add more banks to the diagram, the price would change. The example uses a simple average between two prices to negotiate on a tradable price, and the market price is the average of three interbank prices. Actual pricing algorithms are significantly more complicated, and we have not even considered volume or the spread.

However, it does illustrate how a forex price is created. The major difference between forex and other markets is that on an exchange you can only have one price with two types of players (buyers and sellers), whereas in FX you have multiple exchanges known as an electronic communication network (ECN) or a liquidity pool. To complicate matters, individual banks may participate in multiple ECNs. So it is not always easy to determine which parties are responsible for a particular price creation.

The result of this multinode network is a smoothed price that is considered the market price globally. If any bank offered a significantly off-market price, traders or other banks could easily take advantage of it and have an arbitrage opportunity. Bear in mind this is all happening within seconds, so without the use of advanced computing technology, it would be difficult to follow this activity.

BUY SIDE VERSUS SELL SIDE

In equities, the sell side represents an investment bank that issues a security and sells it to the market, and the buy side represents other investment banks and investors who buy the security in the market from those banks. Foreign exchange is a little different, but a similar relationship exists. In forex, the terms “buy side” and “sell side” are not as appropriate as it is in equities. A better description would be “liquidity maker” and “liquidity taker” — the maker being the banks, and the taker being traders or other banks.

FX convolutes this even more. Sometimes these players will reverse roles, or they may be a maker on one ECN and a taker on another. As there is no standard for how to manage FX order flow, banks and other institutions can become creative and have the ability to structure their order book in many ways. And because this structure is internal and confidential, we can only speculate based on output (which we see in the markets and in public data such as Bank for International Settlements [BIS] surveys and volume reports).

VIABILITY OF ARBITRAGE IN FOREX

Developing any type of arbitrage trading strategy requires the following elements:

- Access to the highest quality price information

- Fast Internet connection at multiple nodes

- Sophisticated computer hardware

- Custom software written to execute the strategy

- Constant updates of the infrastructure

This requires a solid understanding of the involved technologies, but fulfilling these requirements does not guarantee you a profit, either. You could also build up a specific infrastructure that will take time to create, and by the time you can implement it, the types of existing opportunities may change.

But how practical is it? While we don’t have information about how many arbitrage traders there are, we can assume that at least several well-funded and sophisticated groups are trying to take advantage of such opportunities in forex. Not only would you be competing with them, as the market and technology evolve, you would be also competing with infrastructure that is constantly being updated.

PRACTICAL EXAMPLES

The image of Figure 2 was taken on the Currenex interbank platform during a release of nonfarm payrolls. If a trader was quick, it would be possible to click buy and sell and capture the difference in profit because the bid is higher than the ask. Unless you clicked both buy and sell at the same time, which would be impossible if you were trading manually, your risk would be that price would change by the time you clicked the other side. It is possible for the price to change in one second.

If you use an automated system, it would be possible to send a buy and sell order at the same time and capture the price difference. This strategy is near flawless but would have a limit defined by the amount of volume available at that price. This opportunity may only happen a few times a month.

Advanced Books and Courses on Algorithmic & Quant Trading

LATENCY RESTRICTIONS

Given that markets are interconnected globally through the Internet, latency should be considered when developing any type of arbitrage strategy. Arbitrage opportunities may last for only a few seconds, if that. If the latency to your counterparty is 100 milliseconds, and it takes 200 milliseconds to fill an order, the market may have changed during that time, in which case the trade could end up being a loss. Slippage should also be considered. Unless the opportunity has a large spread, a small amount of slippage could turn a seemingly profitable arbitrage opportunity into a loss.

Latency is volatile and should be monitored in real-time. Numerous Internet service providers (ISPs) are involved with a number of routers and network connections. Just because the current ping to your counterparty is 20 milliseconds (ms), that doesn’t mean it will always be 20ms. During a large market event, depending on the bandwidth of their network infrastructure, a large amount of price data could create additional delays. Any arbitrage strategy should incorporate real-time network monitoring as part of the strategy.

FILL RISK

Another risk in arbitrage strategies is that orders may not be filled quickly, if at all. If you needed to use more than one counterparty, there is a chance that one of them may reject your order. In this case, you would have a naked real position in the market that would be subject to traditional profit and loss. If leverage was used, this could be a big risk if the market was moving quickly.

COUNTERPARTY RISK

Any arbitrage strategy requires at least one counterparty to trade with. In the case of multileg arbitrage, it may require more than one. Quality of the counterparty should be considered. There may exist an inverse correlation with the quality of the counterparty and arbitrage opportunities. For example, a big-name forex bank such as JP Morgan likely has a lot of experience, and even their personnel may have some experience with forex arbitrage. They probably have a sophisticated infrastructure, if only because of their large budget. Finally, due to the large amount of liquidity they process, any arbitrage opportunities may be smoothed by their liquidity algorithms.

In contrast, a small underfunded forex brokerage with a small amount of experience and bare-bones infrastructure may provide many opportunities for arbitrage, but these opportunities come with risks:

- Failure to fill one leg of the trade due to technical difficulties

- They can reverse your trades

- They can go out of business.

DIFFERENCES BETWEEN ARBITRAGE AND CORRELATION

Many arbitrage strategies are actually correlations. Traders believe in their mean-reversion correlations so much that they consider them to be arbitrage when actually they are correlations. That is not to say they are not effective, just that it is not fair to call them arbitrage. Traders seek correlations in all markets, but forex correlations are interesting because of the connections between other markets and money markets, which sometimes represent real money flows from one market to another. Some correlations that have been noted by traders are:

- Pair correlations (that is, a move in GBP/JPY is correlated with GBP/USD and USD/JPY)

- Stock markets correlated with certain forex pairs, such as USD/JPY being correlated with US stock markets

- Correlation between certain commodities, especially oil, and the US dollar.

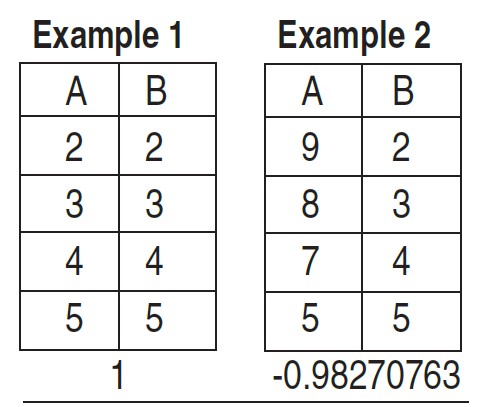

Correlations can be calculated using Microsoft Excel, with any two sets of data (=CORREL). Usually, traders use daily data to calculate correlations, but any two datasets can be used. The result will be a correlation coefficient (a number from -1 to +1) 1 being 100% correlated and -1 being 100% negatively correlated.

In example 1 (as seen in Figure 3), datasets A and B are identical, so the correlation value is 1. In example 2, datasets are almost opposite, so correlation is almost -1. Traders without significant experience or capital/time investment may want to consider trading a correlation strategy as opposed to arbitrage.

CONCLUSION

While price discrepancies have been documented in forex, capturing them may require a large investment in time and money and experience in programming and trading. While arbitrage is alluring, traders should consider the risks and pitfalls associated with this type of trading.

- Joseph James Gelet is the president of Elite E Services, which develops automated forex trading systems and offers managed accounts.