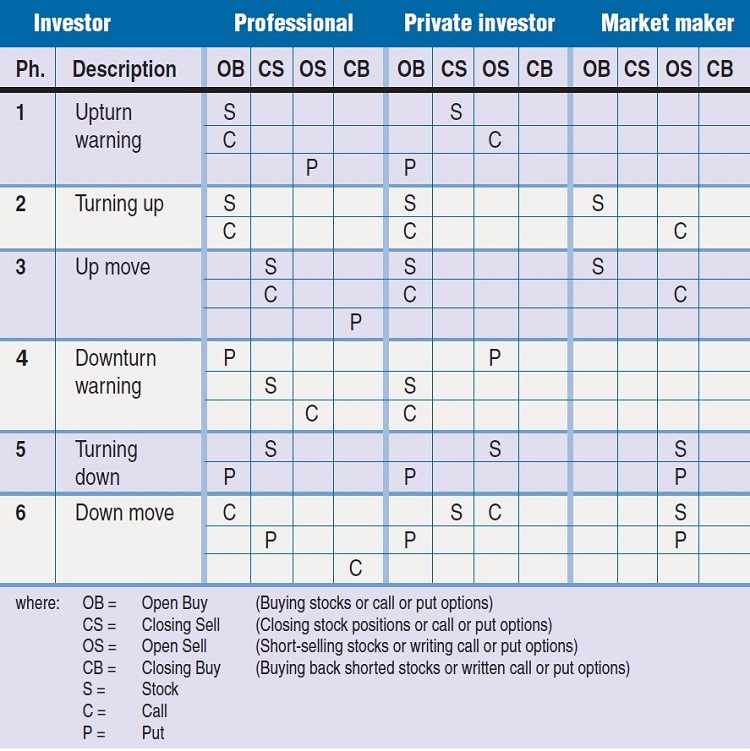

Trading Articles

The Put/Call Ratio And Price Cycles By Sylvain Vervoort

The put/call ratio and open interest can be used as a leading indicator to predict the next index move. In this, the first part of a three-part series, the put/call ratio is defined and the cyclical phases this indicator goes through. I started writing my first book near the end of the previous century. That sounds like such a long time ago! It was only published in Flemish, my native language. A small part was about fundamental analysis, the main part was about technical analysis, and there was an introduction to option strategies. In the part about option strategies, based on the put/call ratio and the open interest, I wrote about my idea of how these two parameters could be used as a leading indicator to predict the next index move.

For a couple of years afterward, I published followup commentary and accompanying data from the European Options Exchange (EOE). Unfortunately, at some point this data stopped being offered anywhere I looked for it and I had to abandon that project, much to my regret. Then in early 2010, I noticed that the put/call ratio of all the CBOE equity options is available at the CBOE website. There, you can find the CBOE equity put/call ratio data from October 21, 2003. That made me think about my earlier work.

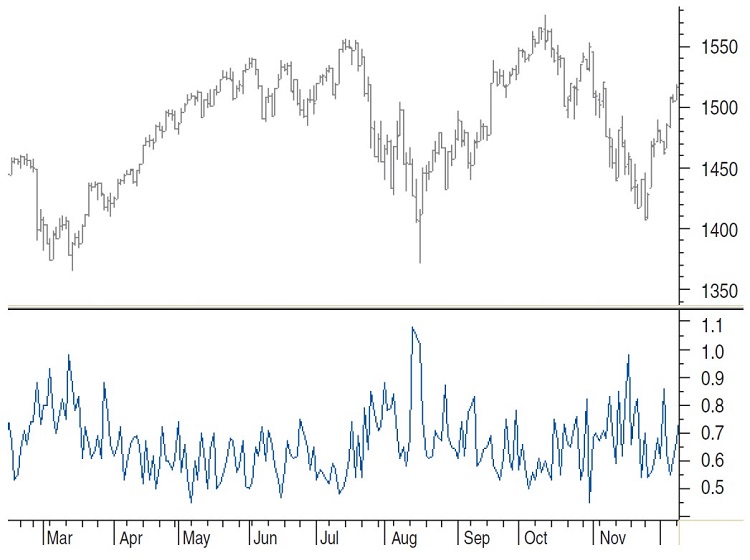

An indicator that uses the put/call ratio has an advantage in that it is not based on the usual price or volume data, and as such, it can be an interesting extra piece of independent price information. Looking at Figure 1, however, where you see a chart of the Standard & Poor’s 500 at the top with the raw put/call ratio data at the bottom, it is evident that we will need some tricks to create a usable indicator.

PUT/CALL RATIO DEFINITION

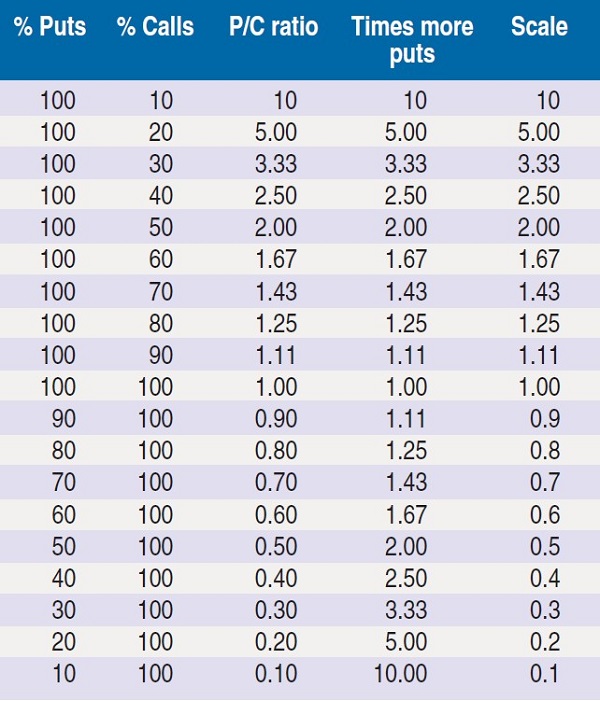

You get the daily put/call ratio by dividing the sum of all put options by all call options traded on all individual CBOE equity option contracts. Important: Do not use the put/call ratio of the index itself; this will not give you a meaningful indicator. The result will be 1 if the number of puts and calls traded are equal. In Figure 2, you can see the resulting scale with varying percentages of puts and calls. If you are using a linear scale for the indicator, you may have to do something with puts that move linearly from 1 to 10 and calls that only move from 0.1 to 1.

But if you look at the Cboe equity option data from 2003 till now, the put/call ratio is rarely larger than 1 or smaller than 0.45. That means that using a linear scale is not a useful item, and that the ratio varies in reality between an equal number of calls and puts and about 2.5 times more calls than puts.

Normally, you will see the index moving up while the put/call ratio is going down. More calls than puts are traded and the call option buyers believe in a further upside movement of the stock price. Conversely, you will see the index moving down with an upward moving put/call ratio. This means more puts are traded, and more put option traders are convinced of a continued move down of the stock price.

CALL AND PUT CONTRACTS

Before we go on, let’s make sure we know precisely what a stock call or put option is:

- The call option contract buyer has the right, not the obligation, to purchase the stock at the strike price until expiration date.

- The put option contract buyer has the right, not the obligation, to sell the stock at the strike price until expiration date.

Whereas:

- The call option contract writer has an obligation to deliver the stock at the strike price until the expiration date.

- The put option contract writer has an obligation to buy the stock at the strike price until the expiration date.

The strike price of an option is the price at which the writer of the option agrees to buy or sell the underlying. The expiration month is the month that the option will expire with an expiration date normally the third Friday of that month. An option contract mostly represents 100 shares of the stock.

PUT/CALL RATIO AND PRICE CYCLES

Phase 1: The put/call ratio up turn warning

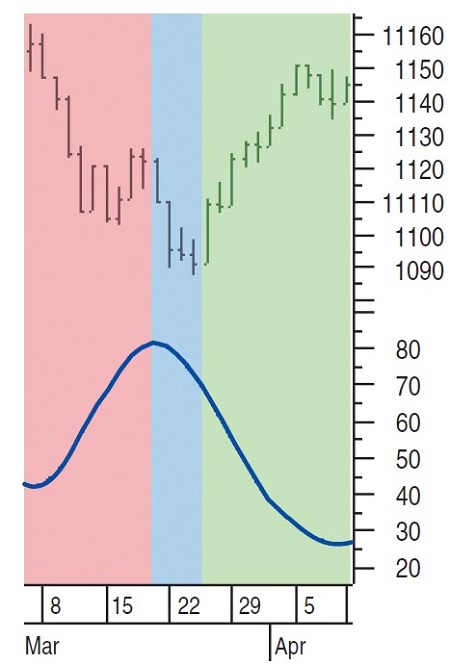

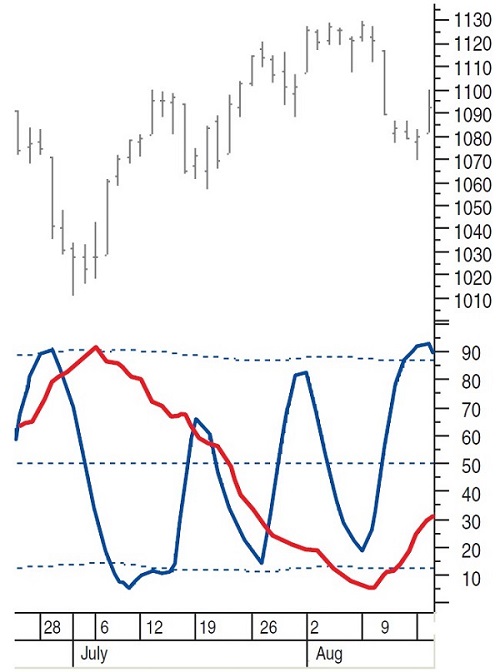

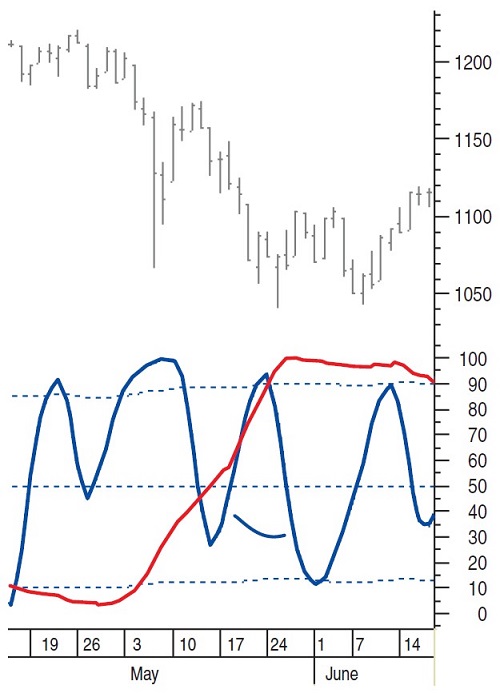

In a normal short-term down move, the put/call ratio indicator will be moving up. In Figure 3, where the indicator is plotted below the index, this price zone is marked in red. In a normal short-term up move, the put/call ratio indicator will move down. This is the green zone in Figure 3.

The most interesting part here is the blue zone, where the short-term put/call ratio starts moving down while the index continues moving down or flat in the downtrend. This is an early warning for an upcoming price reversal. The downward move in the put/call ratio means that more calls than puts are being traded.

What is happening here is that private investors start selling stocks because they lose too much money in the downtrend. Stop-loss levels are broken, while others keep the stock and try to compensate for the loss by writing call options. They are convinced that the written call options will end up worthless as the downtrend continues. Finally, some investors buy put options to protect their stocks and/or simply try to profit from the down-trend.

Others — let’s call them professionals — are picking up the stocks at continuous lower prices and buying the call options written by private investors. They also write the put options bought by private investors. Sounds like the professionals know price is going to move up soon. If that is the case, they will profit by selling the stocks and call options at higher prices and they can buy back the written put options at a lower price, making money on stocks and more money with the options.

Phase 2: The up turn

The put/call ratio is moving down and the index is turning up after a downtrend. This area is marked green in Figure 3. As they keep an eye on fundamental and technical data, professional traders start buying more and more stocks, creating an upward turning point in the index. They are probably also still buying more call options.

Some private investors are buying additional stocks to average down their buying price. Early private investors follow soon and start buying stocks and call options based on technical analysis signals. The writer of the call options is the market maker. He will write covered call contracts, buying the underlying stock. The result of all this buying is a fast upturn of stock and call option prices.

Phase 3: The up move

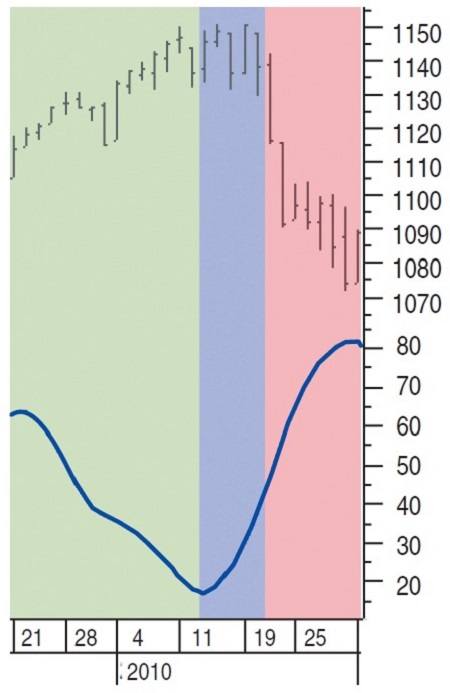

In Figure 4 you can see the red medium-term put/call ratio is moving down and the index is moving up, usually in tune with the short-term (blue) put/call ratio and price corrections. The up move is now well on its way, and more private investors are coming in. They are buying stocks and call options. The professional market participant takes stepwise profit on a small part of his stocks and call options and closes the written put contracts, making more profit buying them back at a lower price. Call options bought by the private investors are countered by the market maker writing covered call options. The overall result is a price up move in the medium term.

Phase 4: The put/call ratio downturn warning

In a normal short-term up move, the put/call ratio indicator moves down. This price zone is marked green in Figure 5. In a normal short-term down move, the put/call ratio indicator moves up. This is the red zone in Figure 5. The most interesting part is the blue zone, where the short-term put/call ratio starts moving up, while the index continues moving up or is flat during the uptrend. This is a warning of an upcoming price reversal. When the put/call ratio moves up, it means that more puts are being traded in the uptrend.

What is happening in this scenario is that private investors holding the covered written “phase 1” call options are not making money in the uptrend. Wanting to keep their stock positions, they start writing put options in order to compensate for the loss of profit because they are convinced these written put options will end up worthless with a higher or flat stock price. Meanwhile, others will be buying stocks and call options trying to profit from the uptrend.

Professionals are selling more of their stocks with increased profit. They buy the put options written by private investors and write call options bought by other private investors. Sounds like the professionals know price is coming down soon. If that is the case, they will profit by selling the put options at higher prices and they can buy back the written call options at a lower price, making more money!

Suggested Books and Courses About Trading Options

Phase 5: Turning down

In this phase, the put/call ratio moves up and the index turns down after an uptrend. This phase is the red area in Figure 5. With an eye on fundamental and technical data, professional traders start selling all of their remaining stocks, creating the downward turning point in the index. They are probably still buying more put options.

Early private investors soon follow, sell their stocks, and start opening short stock positions and put options based on technical analysis signals. The writer of the put options is the market maker. He will write put contracts and open short stock positions to cover his obligation. The result is a fast downturn of stock prices and higher put option prices.

Phase 6: The down move

In Figure 6 you can see the red medium-term put/call ratio moving up and the index moving down, usually in tune with the short-term (blue) put/call ratio and price corrections. The down move is now well on its way, and more and more private investors sell their stocks or write call options to compensate for some of their stock losses, while others buy put options. The professional takes stepwise profit on his put options and closes the written call contracts, making a profit, buying them back at a lower price. Put options now bought by the private investors are countered by the market maker covered by short positions in the stock. The overall result is a medium-term downward price move.

That completes the last cycle, bringing us back to phase 1. Figure 7 shows an overview of all cycles. Next time, in the second part of this series, I will create the put/call ratio indicator (PCRI).

Sylvain Vervoort, a native of Belgium, is a retired electronics engineer who has been studying and using technical analysis for more than 30 years. His book Capturing Profit With Technical Analysis, published by Marketplace Books, was awarded a bronze medal from the 2010 Axiom Business Book Awards in the investing category. The book’s focus is on applied technical analysis, introducing a trading method called Lockit.