Trading Articles

Why Stock Prices Move: Four Core Drivers Explained

In a article titled “Gems Among The Talus,” Thomas Maskell outlined three reasons for stock price moves: growth, earnings, and money flow. He also discussed how those factors might be analyzed using technical analysis. This article continues to explore that avenue of thought and presents another way of thinking about the causes of stock price moves, and also offers four reasons why stock prices move.

WHY AND WHAT?

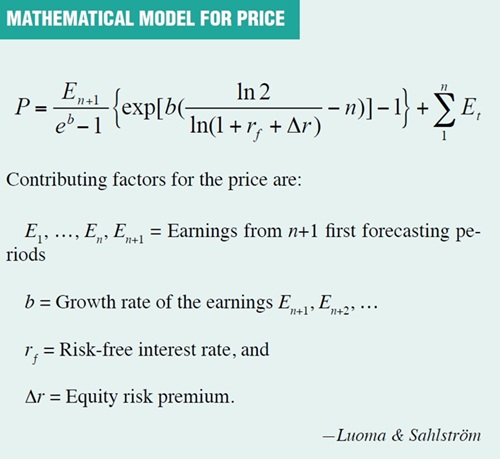

Taking a cue from Maskell’s work, we decided to use a valuation model of stocks to provide a solid base to the analysis. We use the model first presented in S&C in May 2001 and later further developed by Luoma and Petri Sahlström elsewhere. Here are four ways that stock price moves are affected:

- Earnings per share

- Earnings growth

- Risk-free interest rate

- Equity risk premium

The first is earnings per share (EPS). A stock acquires value through its ability to make money for its holders in the present and a promise to do so in the future. Thus, the higher the EPS is, the higher the stock price goes. Future expectations also affect stock prices: for example, the growth rate of the EPS predicts the size. In practice, rapidly growing companies reflect rapidly increasing EPS. This is why earnings growth is second on our list of reasons for stock price moves.

Third on our list is a risk-free interest rate, which is also an important factor in the stock market. It controls price through fixing the interest rate on bonds and other instruments. Companies generally need to obtain finance from the market for investment purposes at some point in their development, and that influences the firms’ EPS and hence stock price. But bonds are also alternative investment objects for stocks, and the interest rate available also influences stock prices.

While the interest rate is low and money is cheap, demand for stocks increases as money flows into stocks. When money is cheap, firms see opportunities for bigger returns; for example, companies may invest in more effective machinery, be able to produce more and, as a result, earn more. Market sentiment is also an important factor. While often mentioned, it is nonetheless difficult to define and measure. Consequently, Maskell adopted the concept of money flow rather than market sentiment, but we prefer to concentrate on equity risk premium, the fourth reason on our list. The basic rule is that if market sentiment is strong, the equity risk premium is small.

There are also other ways that the equity risk premium is affected. However, we define the premium as follows: If the investor buys a stock or other risky security instead of a risk-free security, he or she wants compensation for the risk involved. The equity risk premium is simply the expected extra return, which means the price is adapting in such a way:

Expected return = Risk-free rate + Equity risk premium

A strong market sentiment means that the investor will be pleased with a low equity risk premium. There is also a fifth reason: inflation. However, it has no influence on cross-sectional analysis. In a time series analysis with equal time spans, inflation has the same influence on all stocks and, therefore, it does not make our list. Relationships between price and reasons may be positive or negative, and the key relationships are:

- Positive relationship between earnings per share and price

- Positive relationship between the earnings growth and price

- Negative relationship between the risk-free interest rate and price

- Negative relationship between the equity risk premium and price.

AN EXAMPLE

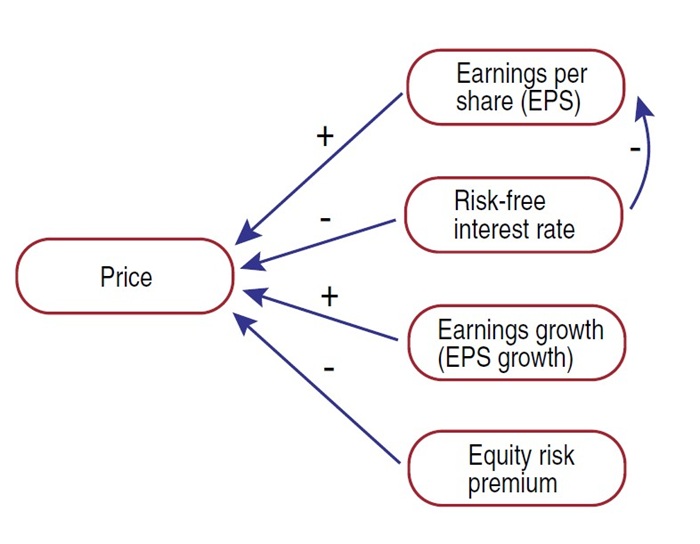

All four reasons have a direct impact on price, but some other reasons are indirect. Figure 1 shows that the risk-free interest rate has a direct impact on the price but also an indirect one through earnings per share. Other indirect impacts are possible as well.

Financial theory tells us if the relationship is positive or negative between factors and price, but we do not know the magnitude of the impact. For example, if an interest rate increases 0.25 percentage points, what will be the change in price? Or if there is a belief that the equity risk premium used in calculating stock value is 0.5 percentage points too high, making the stock undervalued, what would be the effect on the price?

Advanced Books and Courses on Risk Management

To discover the magnitude of the effect, we used Luoma and Sahlström’s valuation model. The mathematical model is presented in the sidebar, “Mathematical Model For Price.” The model uses forecasts to calculate EPS, EPS growth rate, and also equity risk premium, because valuation depends on the present price and expected returns in the future.

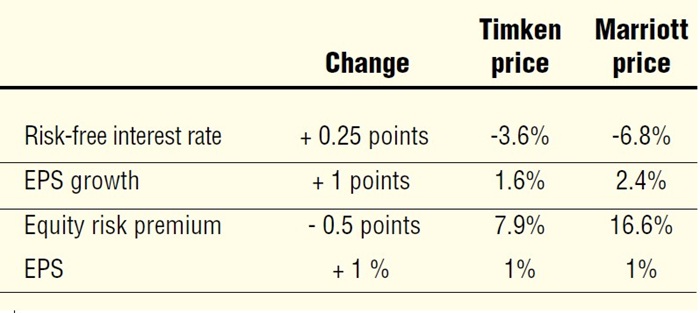

We looked at two New York Stock Exchange stocks, Timken (TKR) and Marriott International (MAR), as an example. Figure 2 presents the calculated effects that the four reasons have on price. The figure shows that interest rate and equity risk premium can have an enormous impact on the stock price. If the interest rate grows 0.25 percentage points, the effect on the price of the Timken stock is -3.6% and for Marriott -6.8%. This is only the direct effect. We were not able to establish the degree of any indirect effect, so these calculations show only the minimum magnitude.

On the other hand, if the risk premium were to drop by 0.5 points, the actual effect on the stock price would be a growth of 7.9% for Timken and 16.6% for Marriott. Changes to EPS and EPS growth do not have any surprisingly great effect on the prices.

ANTICIPATING PRICE MOVES

This study has generated some interesting findings. Most people would likely be surprised to learn that the free interest rate and equity risk premium would have such a strong effect on stock prices. This effect is not so easy to discern in practice, because markets react to changes in interest rates progressively and often before changes are implemented. Traders should be aware of this, however.

The method presented here could provide traders and investors with a tool to estimate the magnitude of changes in advance, something that could have a huge bearing on the way stocks are valued and traded.

- Martti Luoma is professor emeritus of statistics in the Department of Mathematics and Statistics at the University of Vaasa, Finland.

- Annukka Jokipii is a postdoctoral researcher at the University of Vaasa.