Trading Articles

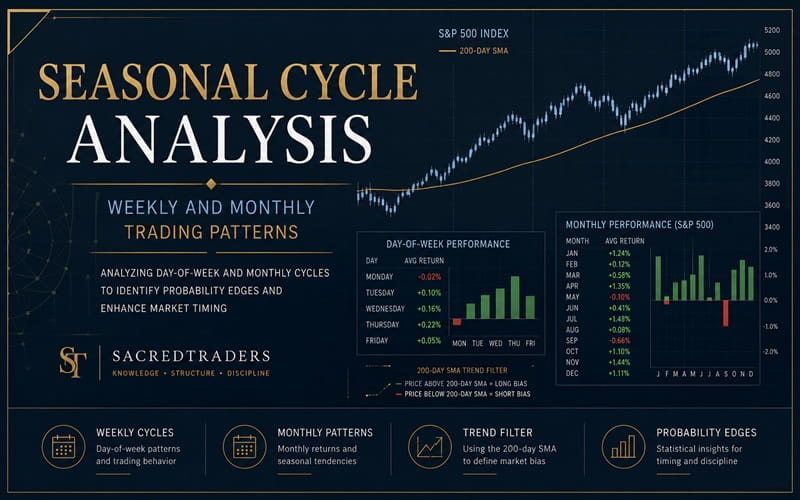

Seasonal Cycle Analysis: Weekly and Monthly Trading Patterns

These two short-term seasonal cycles can give traders an edge. In recent years, making use of the seasonal cycles of various stocks and commodities have become a popular trading technique. For example, “Sell in May and go away” is a popular saying among equity traders, reflecting the tendency of the Standard & Poor’s 500 to experience weakness during the summer months. The “Santa Claus rally” is another example of the yearly seasonal cycle of stocks, reflecting how traders can make use of the year-end market activity.

However, the yearly seasonal cycle is only one of a few that are anchored on dates, and which make up the broader category of seasonals. Here are two short-term seasonal cycles that can provide an edge to traders, using the weekly and monthly seasonal cycles in the S&P 500.

ON THE EDGE

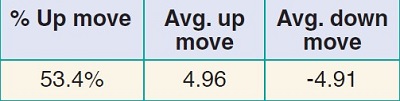

A good starting point to measure the seasonal edge of a particular trading day is to test the average move of any day during a period. Figure 1 shows the average move in the S&P 500 for every day in the period from February 1, 2001, to February 1, 2011. These are the figures against which all other day-to-day moves should be measured against. Only if a day is up more than 53.4% of the time or offers a better than 1.01 reward-risk ratio can it be said to provide an edge for long trades.

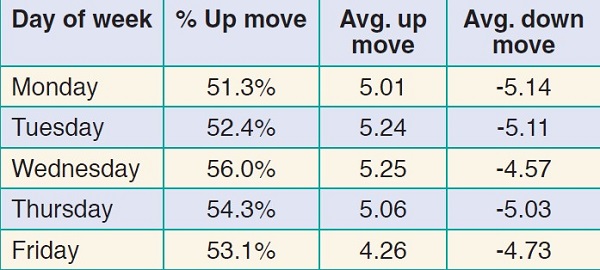

Figure 2 shows the magnitude of day-to-day moves in the S&P 500, measured close-to-close from February 1, 2001 to February 1, 2011. During this exceptionally volatile 10-year period, every day of the week had a better than even chance of being an up day. In particular, Wednesday not only had the highest likelihood of being an up day, it also had the best reward-risk ratio at 1.15. In addition, Mondays and Fridays are the only days with unfavorable reward-risk ratios for long trades, although neither Tuesday nor Thursday is exceptionally favorable.

This information is in and of itself useful to swing traders and daytraders. For example, it suggests that Tuesday near the close is a good time for a long entry, while daytrading with a long bias on Wednesday should provide an edge, assuming that all other factors are neutral. However, this data does not reflect how skilled traders will actually trade. Generally, unless strong evidence of a reversal is present, a skilled trader will want to take long positions only when the underlying trend is bullish.

While numerous mechanisms are available to measure trend, one simple but effective way of measuring the long-term trend of a market is to compare the price of the market to its 200-day simple moving average (SMA). Trading above the 200-day SMA is indicative of a bull market, while trading below the 200-day SMA is indicative of a bear market.

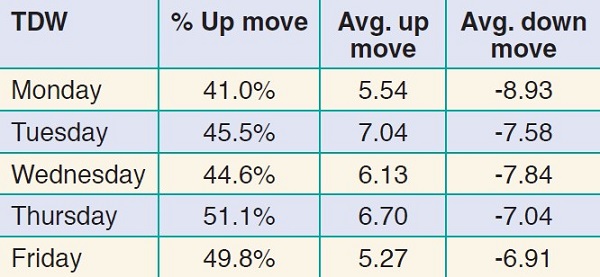

Returning to the weekly seasonal pattern, we would expect that long trades opened up on any day of the week should experience better results if they are opened only when price closes above its 200-day moving average. The actual data bears this out, as shown in Figure 3.

These results are far better than those that can be had by trad-ing without considering the underlying trend. In fact, Monday and Wednesday now show better than 60% up moves and far better reward-risk ratios, with Monday showing a risk-reward ratio of better than 2 to 1. Further, swing traders will gain an edge if they close out long trades on Thursday or early Friday to avoid Friday’s subpar results, all else being equal.

Compare the last set of results with Figure 4, which shows day-to-day moves in the S&P 500 when price closes below its 200-day moving average. As expected, the S&P experiences far worse results on a day of the week basis when it is trading below its 200-day moving average. In fact, when the S&P 500 closes below its 200-day moving average, there is no day that provides an edge for long trades. However, Monday appears to provide an acceptable edge for short trades, with a 59% success rate and a reward-risk ratio of about 1.6 to 1.

While knowing the odds for a particular day of the week can provide an edge, especially when coupled with information regarding trend, we have found that the seasonal pattern surrounding trading days of the month provides an even greater edge. We define a trading day of the month as a day in which active trading takes place, so holidays and weekends are excluded. The seventh trading day of the month is never the actual seventh day of the month, as at least one weekend would have occurred by that day. Figure 5 shows a calendar of January 2011, with the trading days of the month numbered.

Advanced Books and Courses on Market Cycles & Timings

PATTERNS OF CYCLICAL MOVEMENT

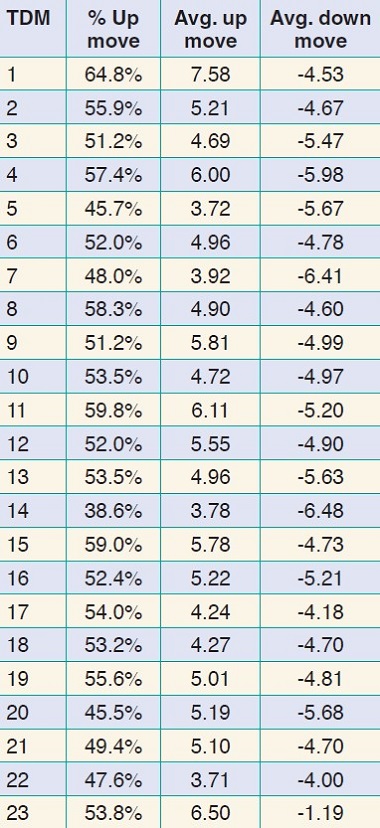

Now that we have clarified our terminology, Figure 6 shows the monthly pattern of day-to-day moves in price of the S&P 500. Note a few important points. First, certain days of the month are, in essence, bullish or bearish. In particular, the first day of the month is up 64.8% of the time and provides a reward-risk ratio of 1.67. In and of itself, going long on the first day of the month would have paid off handsomely over this period.

Days 11 and 15 also provide better than average opportunities for long traders. On the other hand, day 14 provides poor odds for long trades, which, of course, makes it a good day to be short. It is down 61.2% of the time and for short trades, it provides a reward-risk ratio of 1.7. Similarly, days 5, 7, and 20 provide better than average opportunities to go short.

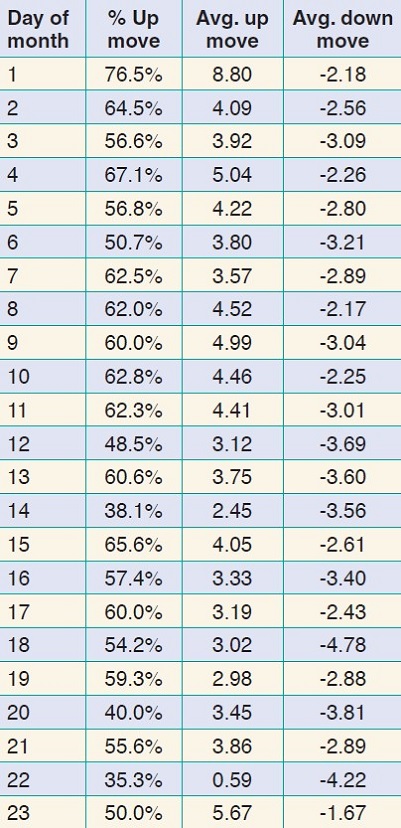

As stated earlier, skilled traders will usually place their trades in the direction of the trend. Accordingly, Figure 7 shows the monthly pattern of daily moves in price of the S&P 500 when price closes over its 200-day SMA.

As with the day of the week results, these results are far better for long traders than the general results set forth earlier. For example, day 1 provides impressive results, with an up close 76.5% of the time and a better than 3-to-1 reward-risk ratio. In addition, 11 days have an up close more than 60% of the time, with day 4 also providing a better than 2-to-1 reward-risk ratio. However even in this bullish scenario, several days are still outright bearish. Days 12, 20, and 22 all close higher less than 50% of the time, and day 14 is generally a day to avoid being long, with only 38.1% higher closes and an alarming reward-risk ratio of only 0.68.

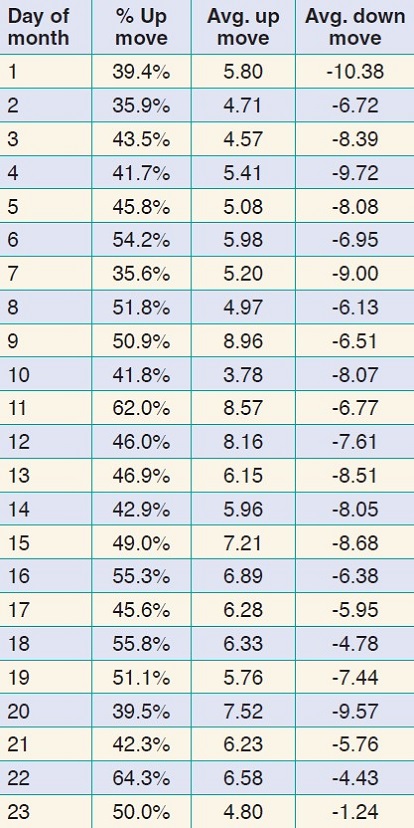

To complete our brief survey of short-term seasonal effects, Figure 8 shows the monthly pattern of day-to-day moves in the S&P 500 when it closes below its 200-day moving average. The S&P 500 provides very few opportunities for long traders when it is trading below its 200-day SMA. The best trading days of the month for long trades are 11 and 22, although neither provides even a 1.5-to-1 reward-risk ratio.

However, opportunities to go short abound. Day 1, which is generally quite bullish, provides a 60.4% win rate for short trades with a 1.8-to-1 reward-risk ratio, while days 2, 7, and 20 also provide a better than 60% probability of a lower close. Surprisingly, day 14 actually provides somewhat better results when the S&P 500 trades below its 200-day moving average than when it trades above its 200-day moving average, although the overall results for day 14 are still heavily slanted to the short side.

We encourage you to use this information for the S&P 500 to sharpen your own trades. On an emotional level, traders often cling to their preferred strategies. Even when those strategies no longer fit current market conditions, traders tend to remain with their routines. However, just as a garden needs regular weeding to flourish, your trading approach also can benefit from stepping out of your comfort zone to plant the seeds of effective new strategies.

APPLYING IT

We use this information as a tiebreaker when other tools do not provide a clear sense of direction for the market. We use the seasonal data when the market trades above its 200-day SMA whenever we estimate that the underlying trend is bullish. We use the seasonal data when the market trades below its 200-day SMA whenever we estimate that the underlying trend is bearish. We use the all-encompassing data whenever we believe the trend of the market is neutral. The code for this strategy can be seen here, “EasyLanguage Code For Weekly And Monthly Cycles.”

While we have given information for the seasonal patterns that reflect recent trading activity, these patterns will likely shift over time. For example, Tuesday was a much more bullish day in the 1980s and early 1990s than it has been recently, and Thursday has been more bearish during certain periods. You can update this information periodically to keep abreast of any change in the underlying seasonal patterns, as well as generate information for other markets you are interested in.

- Krista Sherinian is a Naperville, IL–based psychotherapist who specializes in helping traders reach their maximum potential by resolving psychological issues that affect their trading. Konrad Sherinian is an intellectual property attorney and private speculator.